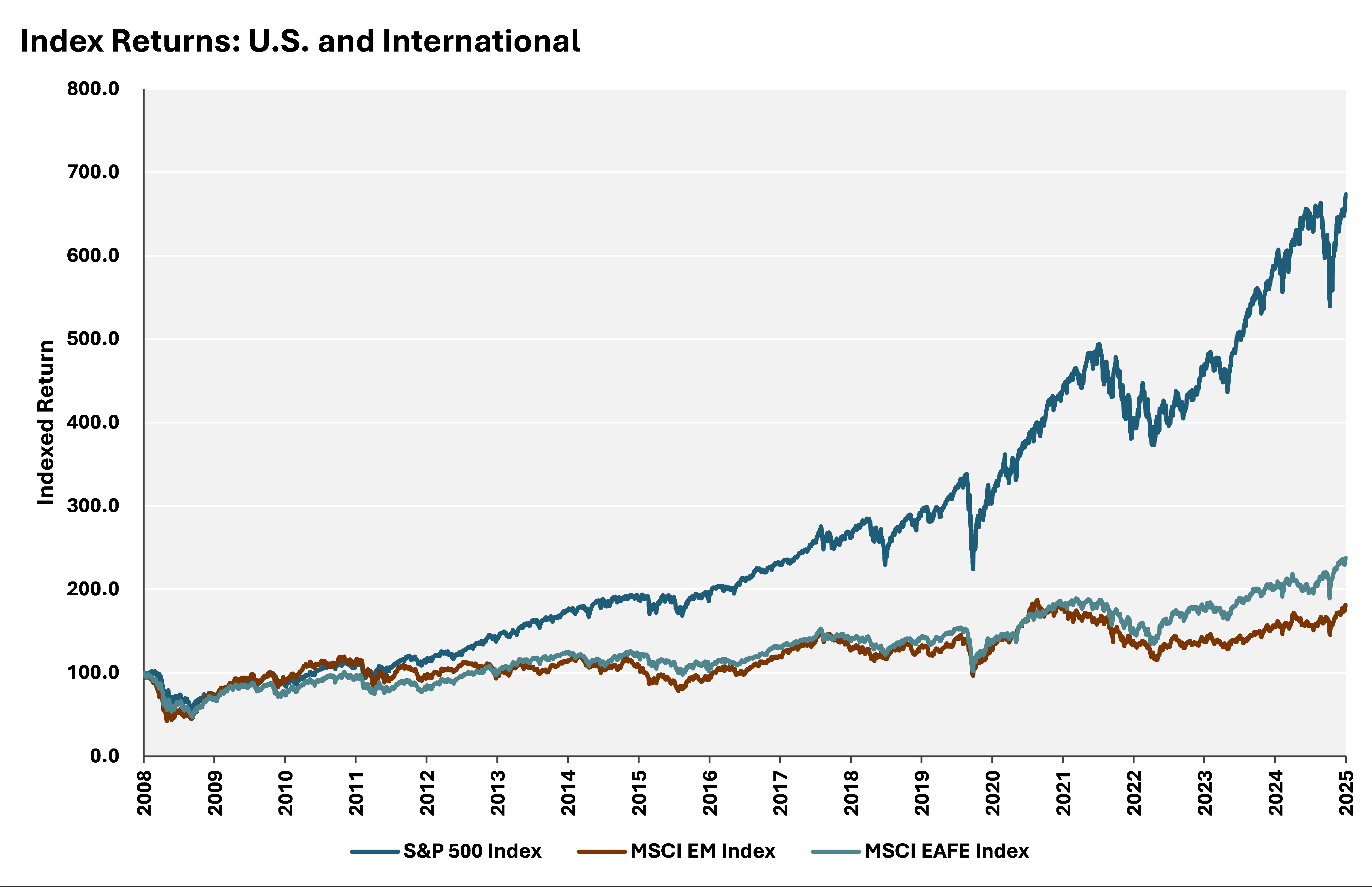

For generations, “American Exceptionalism” has been used to emphasize the United States’ advantages compared to other countries, particularly its democratic system and the individual freedoms its citizens enjoy. The concept has taken on an additional meaning in recent years, however, and highlights the sustained outperformance of U.S. financial markets, especially relative to global counterparts. For context, the U.S. now accounts for roughly 72% of market capitalization in the MSCI World Index, up from roughly 50% in 2010. But so far in 2025 international market returns have outpaced the U.S. The combination of tariff-related policy uncertainty, the potentially inflationary and growth effects of tariffs, immigration policy, and lower taxes appear to have caused investors to look internationally. The picture was further complicated by historic rallies in gold and Bitcoin and a significant drop in the value of the U.S. dollar – its worst six-month stretch in over 50 years. The sudden, though brief, shift in market leadership away from the U.S. has sparked questions about whether there could be a longer period of outperformance ahead for international stocks.

To put the performance into perspective, through the first six months of 2025, developed market equities (ex-U.S.) as measured by the MSCI EAFE (Net) Index had risen 19.5%, emerging market equities as defined by the MSCI Emerging Markets (Net) Index rose 15.3% while the S&P 500 was up 6.2%. On the other hand, gold rallied 25.4% and Bitcoin appreciated by 17.1% in contrast to the U.S. dollar’s 10.8% decline. While these numbers barely dent the superiority of U.S. market returns long-term, the shift in investor sentiment is worth noting.

As discussed, the U.S. vastly outperformed international equity markets in the 15 years prior to 2025. The robust performance has been primarily driven by fundamentally superior earnings growth. Per J.P. Morgan, U.S. companies have grown earnings by 6.3% annualized from mid-2008 to 2024, compared to 1.6% in developed markets (ex-U.S.) with corresponding annual stock market returns of 11.9% and 2.8% respectively. Emerging markets saw earnings grow only slightly better than developed markets (ex-U.S.) and those markets returned 6.3% annualized over the same timeframe.

Earnings growth in the U.S. was however driven in large part by technology companies. Between mid-2008 to the end of 2024, earnings in the technology sector grew by 571%, while its valuation multiple expanded by over 90%, pushing it to become the largest sector within the S&P 500 at 33% of the index. When including companies like Netflix, Google, Meta, and Tesla – four of the “Magnificent 7” – the combined weight moves to roughly 45% of the index. While these companies have significant moats, such concentration at the index level is rare and it bears watching.

The higher earnings growth also led to a significant expansion in valuation multiples. Valuations for the U.S. and developed markets were both relatively similar with the S&P 500 at a price-to-earnings ratio of 11.3x and the MSCI EAFE Index trading at 9.9x. At the end of 2024, valuation multiples for the S&P 500 grew to 21.5x while the EAFE was trading at 13.7x forward earnings. In comparison, the MSCI Emerging Markets Index traded at 12.2x at the end of 2024.

Looking outside the U.S., many economies are showing some green shoots. Lower government deficits, healthier savings rates, and less inflationary pressure than in the U.S. – conditions that allows for more accommodative monetary policy. Combined with new geopolitical realities, such policies could very well cause an investment cycle abroad, which should lift earnings growth.

In emerging markets, continued policy reforms, generally stable currencies, and a potential bottoming of economic conditions in China should assist a recovery in earnings growth as well. Importantly, future earnings growth outside the U.S. is expected to be less concentrated and less reliant on a single sector like technology. In total, while the U.S. will still see higher earnings growth compared to developed markets, the growth-gap is likely to narrow. When combined with attractive valuations, the case for international allocations is strengthening.

Nonetheless, it would be premature to write off U.S. financial markets; the country’s deep capital pools, entrepreneurial culture, and strong institutions remain powerful advantages. Yet, for investors, the prudent path from a risk management perspective is to have a more balanced, globally minded investment approach in the years to come.