The Federal Reserve’s Open Market Committee (FOMC) opted to leave the federal funds target rate unchanged at 2.25 percent to 2.50 percent at their June 19th meeting. At the same time, they released a “dovish” statement implying they may cut short-term interest rates in the very near future. The fixed income markets responded positively to the news, which leads us to the topic of this month’s blog post.

The Fed’s Dual Mandate

The Federal Reserve has a dual mandate to maximize employment while maintaining stable prices. Going into this latest meeting, these objectives were largely achieved. The unemployment rate stood at 3.6 percent (the lowest since the Eisenhower administration) while recent inflation readings were moderate at about 2 percent on an annual basis, right on the Fed’s target.

The Concerns

The obvious question is, if things are going so well, why did the Fed choose to appear more dovish? In a word, “uncertainty.” Uncertainty about “global economic and financial developments.” This was the wording used in their May statement and, although it was removed from their June statement, it appeared again in Chair Jerome Powell’s post- meeting press conference. And while hard economic data remains constructive, survey data (inflation expectations and business confidence) have recently weakened. The Fed was concerned enough to commit to, “monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.” In a nutshell, the Fed is data dependent (shouldn’t they always be?) and currently more inclined to cut interest rates than raise them.

The Market Reaction

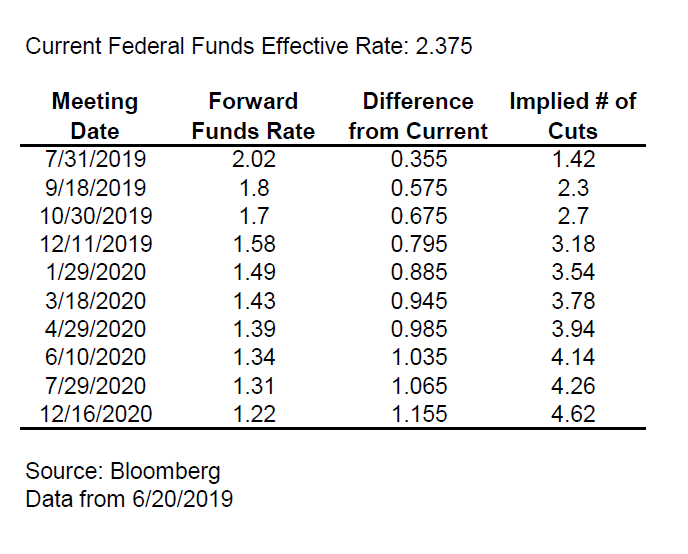

The bond market cheered the Fed statement. The ten-year Treasury note yielded 2.10 percent prior to the Fed’s meeting and subsequently rallied to 1.97 percent, the first time the yield has dropped below 2 percent since October of 2016. More dramatically, the futures market built in numerous short-term interest rate cuts over the next few quarters, as reflected in the table below.

Bond market participants anticipate at least three quarter-point (0.25 percent) rate cuts before year end, and as many as two more in 2020. Many Wall Street analysts now expect a 0.50 percent cut on July 31, 2019.

Has the Market Overreacted?

We think so. Inflation does not appear to be as low as purported, while the economy and employment still appear resilient. There are many inflation statistics to choose from and most show a rate of near 2 percent or higher.

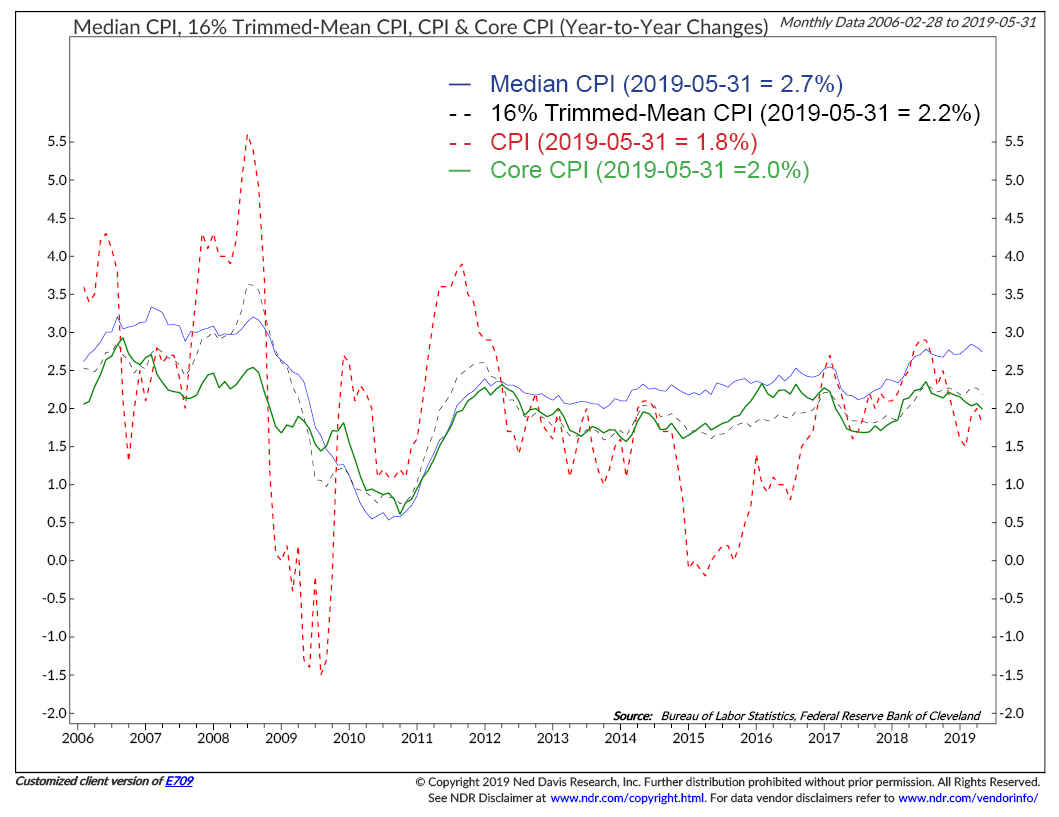

The chart above shows four common inflation statistics. Three of the four are currently at or above 2 percent. Since the era when Alan Greenspan was Chair, the Fed has preferred the Personal Consumption Expenditures Indices (PCE). The PCE indices are not on this graph, but they are currently running at 1.5 percent and 1.6 percent. The Dallas branch of the Federal Reserve makes further adjustments to the PCE and has arrived at 2.0 percent. It is believed that the inflation measure produced by the Dallas Federal Reserve is now the Fed’s favorite. To muddle matters further, some survey and market-based results are at 2.0 percent, or lower. The point is, there is enough variability in the inflation numbers to imply a current rate of 1.5 percent to 2.7 percent. Together, these statistics cluster around 2 percent, right at the Fed’s target, suggesting there is no compelling case for easing.

Trade disputes have taken a prominent role in the news since September 2018. The Fed ignored the disputes, political uncertainty and a government shutdown until stock market volatility drove the S&P 500 down almost 20 percent, from 2,930 to 2,347, in late December. When the Fed did act it was to forgo additional rate hikes and declare they would be “patient.” Now, with the S&P 500 at an all-time high, “uncertainties” have compelled a dovish Fed, and Wall Street forecasts even more dovish rate cuts. While these projections may ultimately prove prescient, they are hard to support with today’s hard statistics.

Conclusion

We believe that the bond market has built in more rate cuts than the Fed may provide. Disappointment over the path of the funds’ rate could then lead to an overall rise in interest rates. The current reward for investing in bonds, that is the prevailing level of rates, is low. On balance, the rewards are not commensurate with the risks and we are cautious fixed income investors.